psneeld

Guru

For Fiona there was hurricane watches for USVI, PR, Florida, Georgia, SC. Warnings about the same. TS watches a small bit bigger and warnings a slight bit smaller. Any would serve the language in most policies. She was a geographically a big storm as well as strong. Even up here our seas were effected as she passed by on her way to Canada. To my mind that’s big. Multiple states and countries. Grandson got a kick watching the waves break over the local sea walls.

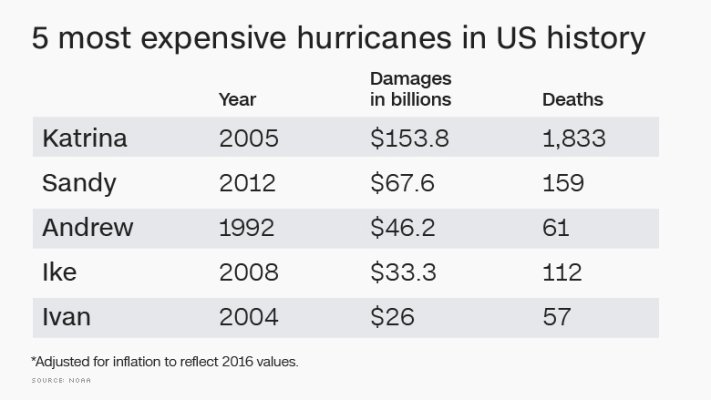

In comparison Sandy was small.

Not sure what the finals are and nothing from Canada yet, but the damages in the Caribbean for Fiona were estimated at 4B.... a bit down the lists.

Sandy was called "Superstorm Sandy"

https://www.britannica.com/event/Superstorm-Sandy

Superstorm Sandy

Superstorm Sandy, also called Hurricane Sandy or Post-Tropical Cyclone Sandy, massive storm that brought significant wind and flooding damage to Jamaica, Cuba, Haiti, the Dominican Republic, The Bahamas, and the U.S. Mid-Atlantic and Northeastern states in late October 2012. Flash flooding generated by the storm’s relentless rainfall, high winds, and coastal storm surges killed 147 people and produced widespread property damage in the areas in its path.

Attachments

Last edited: